Investing in cryptocurrencies can be extremely lucrative. Some people have become millionaires by doing so. However, choosing the one undervalued token that is going to 10x or 100x in value in the next five years is a difficult task.

Dollar cost averaging, which is now available on the SwissBorg app thanks to our new Auto-Invest feature, is a simple investment strategy that any investor can use to build wealth over time, without having to spend hours investigating and agonising over individual investments.

In this article you will learn what dollar cost averaging is, why it is a good investment strategy (especially for beginners!), and you will get some examples that will explain to you how you can implement the strategy straight away.

What is dollar cost averaging?

Dollar cost averaging is a simple and powerful investing strategy. Rather than finding the perfect moment to buy and sell an asset, dollar cost averaging simplifies investing by focusing on investing a fixed amount of money into your portfolio at regular intervals.

Dollar cost averaging is especially useful in the crypto market, where prices are extremely volatile and timing the market is extremely difficult. Therefore, this strategy can minimise your risk, while maximising your exposure to the market. By spreading out your investments over time, fast price movements won’t affect you as much, as the cost of your investment will be averaged out over time. When the market is going up, your portfolio is increasing in value. When it goes down, if you continue investing, you are gaining more assets at a discount.

The concept of dollar cost average was first created by Warren Buffett’s mentor Benjamin Graham, and this concept lies under Warren Buffett’s famous compound investing. While the stock market is a nice investment vehicle, applying this concept to the crypto market can give you even greater benefits since the market grows even more exponentially than the stock market, with many pioneering projects being launched.

Dollar cost averaging in the crypto market

We’ve now established that dollar cost averaging is simply investing in a market or asset over time, rather than trying to find the perfect moment to buy or sell an asset. But how does it work in practice?

With dollar cost averaging, you have a set budget at a set interval that you invest in a certain asset (or across your portfolio).

For example, let’s assume you invest €1,000 on the 7th of each month into the fictive ABCoin. The price of the coin always bounces around, like any asset, which means that each month, your €1,000 will buy a different number of coins.

In January, the price of ABCoins was €10, so you were able to buy 100 coins. In February, the price dropped to €5, so your €1,000 bought you 200 coins. Then in March the price went up to €20, meaning you could buy another 50 coins. Overall, you would get 350 ABCoins for €3,000, at an average price of €8.50 per coin.

Now let’s look at if you’d made a one-time purchase of €3,000 in any one of those months, and how many ABCoins you would have as a result:

- €3,000 purchase in January = 300 coins

- €3,000 purchase in February = 600 coins

- €3,000 purchase in March = 150 coins

When looking at these numbers, it seems like the best approach would have been just to buy the coins in February, and experience even higher growth once ABCoin’s price increased in March.

There are two problems with this approach:

Problem one, is that you have no way of knowing how the market will behave in the short term. If you invest in a crypto with good fundamentals, you might be able to predict that the price will increase over the long-term, but it’s very hard to predict what will happen in the next week or month.

If you take this approach, of saving your money until the price hits its lowest, you could find yourself waiting for a long time for what you believe will be the all-time low, if the price gets there at all (because remember that while it’s easy to look back on a crypto’s price history and point out the low points, at the time it’s very hard to know when the market has bottomed out). This is a time when you could have been building your crypto portfolio and growing your wealth.

Problem two is that you might not have €3,000 to invest in one go. Most people have income that is paid at regular intervals, such as a monthly salary, which means it’s simple to set aside a small amount each time we get paid to put towards our investments. In the previous example, by the time the low hit in February, you would have only had €2,000 to invest (based on the schedule of putting aside €1,000 each month), so it wouldn’t have been possible to invest the full €3,000 at once.

Today, it’s very easy to say, “I should have invested €10,000 in Bitcoin when it crashed in March 2020.” But did you have that much free money available to invest at the time? If not, investing a small amount each month, even as the price goes up, is a better approach then putting aside your money in the hope that there will be another crash, which may never happen.

The challenge of trying to time the market

Looking at the current crypto bull run, some people might think dollar cost averaging is a waste of time. Why would you just invest a little at a time, when you could invest a lump sum and watch your investment increase in value?

As mentioned above, there are a number of problems with this.

The first is that it’s very difficult to predict the bottom of a market when you’re in the middle of it, so you could find yourself constantly waiting for the best time to invest in crypto, and not end up investing at all.

The second is that trying to predict the best time to buy is very time consuming, as you research different projects, follow regulatory updates, perform technical analysis, and follow the major crypto publications and influencers. If you already have a job, a family and hobbies, how will you make the time to do this?

The third problem is the level of emotional stress trying to time the market can cause. If you’re constantly watching the price change, you might find yourself worrying that you’d missed the perfect moment to invest, and criticising yourself for not investing earlier.

The fourth problem is that this approach assumes you will have a lump sum available at one time to make a single investment. As I discussed above, many people who are getting paid a regular salary will be putting aside a certain amount each time they get paid, rather than having a lump sum that’s ready to be invested when the moment’s right.

However, even if you do have a lump sum waiting for the perfect entry price, what happens after you invest it? By focusing on buying at a single point in time, it’s easy to get into the mindset of not wanting to buy more of a crypto if its price goes up, and this means your holdings never grow over time.

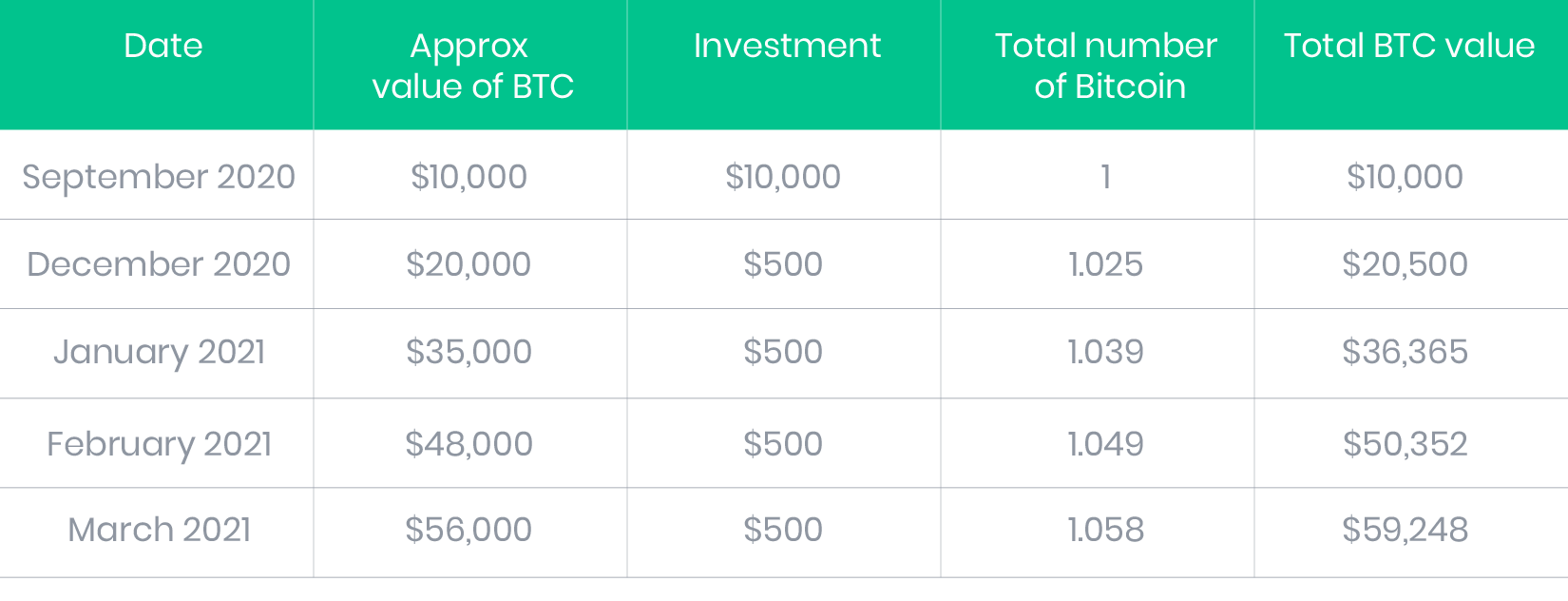

Let’s look at Bitcoin as an example. If you’d bought one Bitcoin at $10,000, when the price jumped to $20,000, you might have said it was too expensive to buy more. In any case, by April 2021 your $10,000 would have increased to nearly $60,000, so you’re doing pretty well. The problem is, if you keep waiting for the price to drop below $20,000 before you make another investment, you aren’t giving yourself the opportunity to continue growing your investment.

If you made a one-time purchase of Bitcoin at $10,000, by mid-March of 2021 you would have about $56,000. But, if you made a one time purchase of Bitcoin when it was priced at €10,000, and then invested $500 a month between December and mid-March, here’s how your investment would have grown:

So over the four-month period, you would have added an extra $2,000 to your existing Bitcoin investment, buying an extra 0.058 Bitcoin. By March, just that $2,000 contribution would have increased to $3,248, bringing your total investment to $59,248.

As you can see, while the gains using the dollar cost averaging method were not as exponential as the original funds you invested, they allowed you to continue adding to your portfolio over time. This gave you the opportunity to add an extra $2,000 to your investment - $2,000 that you might not have had available back in September - and it led to the total value of your portfolio increasing more than it would have if you had stopped with your initial investment.

Why is dollar cost averaging a good investment strategy?

“I don’t believe all this nonsense about market timing. Just buy very good value and when the market is ready that value will be recognised.”- Henry Singleton

As you can see, there are a number of benefits to dollar cost averaging in crypto:

- You remove the pressure of having to time the market perfectly. Instead, you have a certain sum that will be invested each week/fortnight/month and you trust that if you invest in projects with strong fundamentals, those investments will increase over time.

- You benefit from dips in the market, which allow you to buy more of your favourite cryptos at a discount, and lower the average cost of the tokens you hold (increasing the value of any price increase across your holdings).

- You take emotion out of your investments, as FOMO (fear of missing out) is very common among crypto investors, and it can lead people to make poor investment decisions.

- Dollar cost averaging encourages a long-term investing mindset, which will lead to long-term benefits.

Going slow and steady lowers your risk. If you buy everything at one price, your entire investment is at risk if the price drops. If you buy over time, the price of your investment will be averaged over that time, and a price is more likely to rise above long-term averages.

It’s always just a matter of having time in the market rather than trying to time the market.

How to start dollar cost averaging with SwissBorg

The SwissBorg app gives you the opportunity to invest in cryptos with strong fundamentals for the best price, and it can easily be used in a dollar cost averaging strategy with our new Auto-Invest feature. Once you have downloaded and registered in the app:

- Go to Auto-Invest from the Invest tab

- Choose the asset(s) you want to invest in over the long term. (For me, this is the CHSB token!)

- Select how often you want to invest: daily, weekly, every other week or monthly

- Choose the source of funds for your investments.

Tip: If you plan to use a FIAT currency you can automate a monthly bank transfer to the SwissBorg app each month after you get paid to be sure your account is properly funded for the recurring investments. - Define a specific sum you want to invest. Look long-term, for at least six months. This should be an amount you can afford after your essential expenses are covered.

- Reap the benefits of long-term exposure to a growing market, reducing the risk of investing too much money at the wrong time.

Key takeaways

- Dollar cost averaging is a simple and robust investment strategy that involves investing a specific amount in specific assets on set intervals.

- This strategic approach will prime your investor mindset with confidence and help prevent emotional investing.

- This approach will also allow you to continue growing your portfolio over time, rather than constantly waiting for a price crash that might not happen.

- Remember, time in the market is always better than timing the market!

Disclaimer: The information contained in or provided from or through this article (the "Article") is not intended to be and does not constitute financial advice, trading advice, or any other type of advice, and should not be interpreted or understood as any form of promotion, recommendation, inducement, offer or invitation to (i) buy or sell any product, (ii) carry out transactions, or (iii) engage in any other legal transaction. This article should be considered as marketing material and not as the result of financial research/independent investments.

Neither SBorg SA nor its affiliates (“Entities”) make any representation or warranty or guarantee as to the completeness, accuracy, timeliness or suitability of any information contained within any part of the Article, nor to it being free from error. The Entities reserve the right to change any information contained in this Article without restriction or notice. The Entities do not accept any liability (whether in contract, tort or otherwise howsoever and whether or not they have been negligent) for any loss or damage (including, without limitation, loss of profit), which may arise directly or indirectly from use of or reliance on such information and/or from the Article.