Anyone who is deep in crypto or even just dabbles in it will tell you that the last few weeks have been a rocky ride. A depeg or two, record-breaking price drops and more all contributed to a somewhat unexpected market crash we are still feeling the effects of. But, the recent volatility in the market has made two things very clear:

- Stablecoins come with their fair share of risk (some more than others).

- Most people are not aware of the risks.

Thanks to this lack of information, many suffered a significant loss of funds and doubts surrounding the stability of pegged digital assets have dramatically increased.

As we at SwissBorg are very dedicated to protecting our users and enabling them to invest in crypto the smart way, we want to educate those users about the risks of investing in stablecoins and other assets - an effort that we started well before the latest UST crash.

Just last month, we published a post exploring the risks of UST and other stablecoins . Prior to that, we covered a range of topics, including the differences between USDC and USDT.

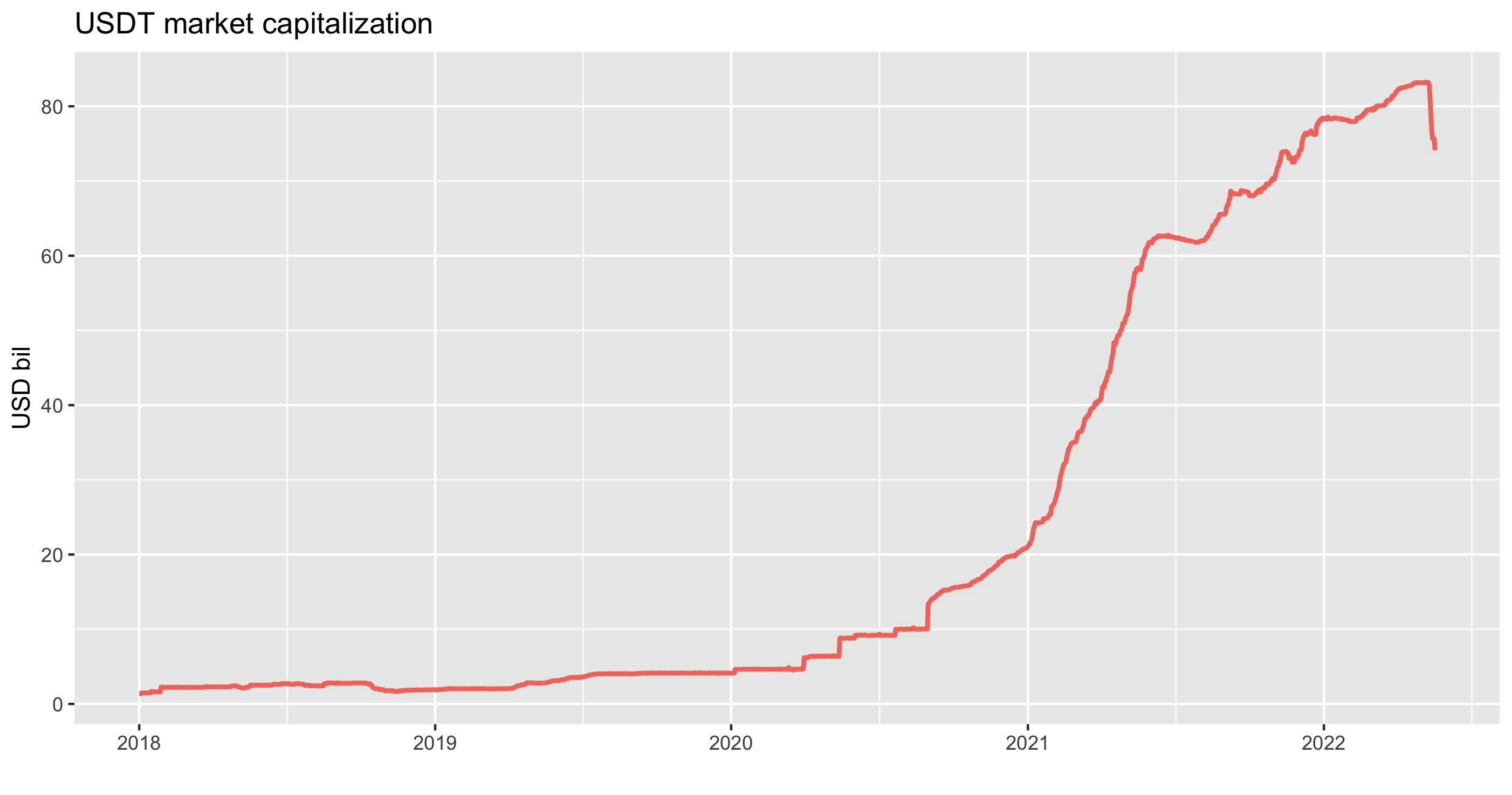

In this article, we will tackle USDT (Tether) , a stablecoin with the biggest market cap of a whopping $74,149,779,864 at the time of writing. If you want to learn more about USDT's creators, its issuing process, risks, and more, follow along with this article!

Who created USDT?

Behind the most widely used stablecoin stands a company named Tether Holdings Ltd.

While not much information on Tether Holdings Ltd is available, what is publicly known is that this is a private limited company based in the British Virgin Islands that enables the conversion of USD into a virtual/crypto version of it - USDT.

The issuing of USDT by Tether Holdings Ltd is done in the following manner:

- An investor wants to convert some of their USD into USDT.

- Tether Holdings Ltd, in exchange for a deposit of, let's say, 100 USD, credits the investor's crypto wallet an equal amount of USDT.

- In theory, Tether Holdings Ltd holds on to the USD so it can return the money to the investor in case they want to convert their USDT back into fiat.

- As long as the investor has the 100 USDT in their crypto wallet, they rest assured that they can at any time go back to Tether Holdings Ltd and redeem each USDT for 1 USD.

The above process also explains USDT's peg to USD.

The importance of USDT (and other stablecoins)

Despite the great popularity they enjoy, many still get puzzled by the purpose of stablecoins. Thus, a question that often arises is, "why in the world of decentralised virtual currencies would I want something linked to a centralised currency like the US Dollar?"

While a detailed answer would require a separate article, the following points might help explain the use and importance of USDT as well as other stablecoins:

- Stablecoins facilitate the trading of USD-priced tokens without the need to rely on banks. This is very useful as banks are often afraid of doing business with crypto companies (e.g. crypto exchanges), especially foreign ones and will not allow them to open an account.

- Stablecoins like USDT are used by crypto traders who want to invest their money through crypto exchanges and easily go in and out of different investments without paying high fees to cash out into USD.

- Stablecoins are open, global, and accessible 24/7 to anyone using the internet. They are also fast, cheap and secure to transmit.

- Coin/token prices are generally shown in USD, meaning it is the baseline currency used to buy/sell them.

USDT Risks

Now that we have gone over how USDT is issued and why we use it, it's crucial we talk about the risks associated with it. Knowing these risks will enable you to decide if USDT is an asset fit for your investor profile and recognise the warning signs of a potential USDT crash.

Reserves

The mechanism implemented by Tether Holdings Ltd in which it holds on to the USD given by investors is what helps create its dollar holdings referred to as "reserves". These reserves ensure that USDT is pegged to USD.

Tether Holdings Ltd initially claimed that "every Tether is always backed 1-to-1, by traditional currency held in our reserves".

This statement was later changed in February 2019 to "Every Tether is always 100% backed by our reserves, which include traditional currency and cash equivalents and, from time to time, may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities".

The new statement shed light on one thing - Tether Holdings Ltd is lending from its reserves, therefore putting them at a potential risk.

Little information is provided explaining what exactly makes up the reserves, and one can't exactly know the maturity of the loans, types of metal, and other details if they look at Tether Holdings Ltd's description of them:

Which bank holds these reserves is yet to be determined.

Adding to this is the fact that the first audited report of the reserves was done only in February 2021 by an unknown firm based in the Cayman Islands, serving as an independent auditor.

Liquidity

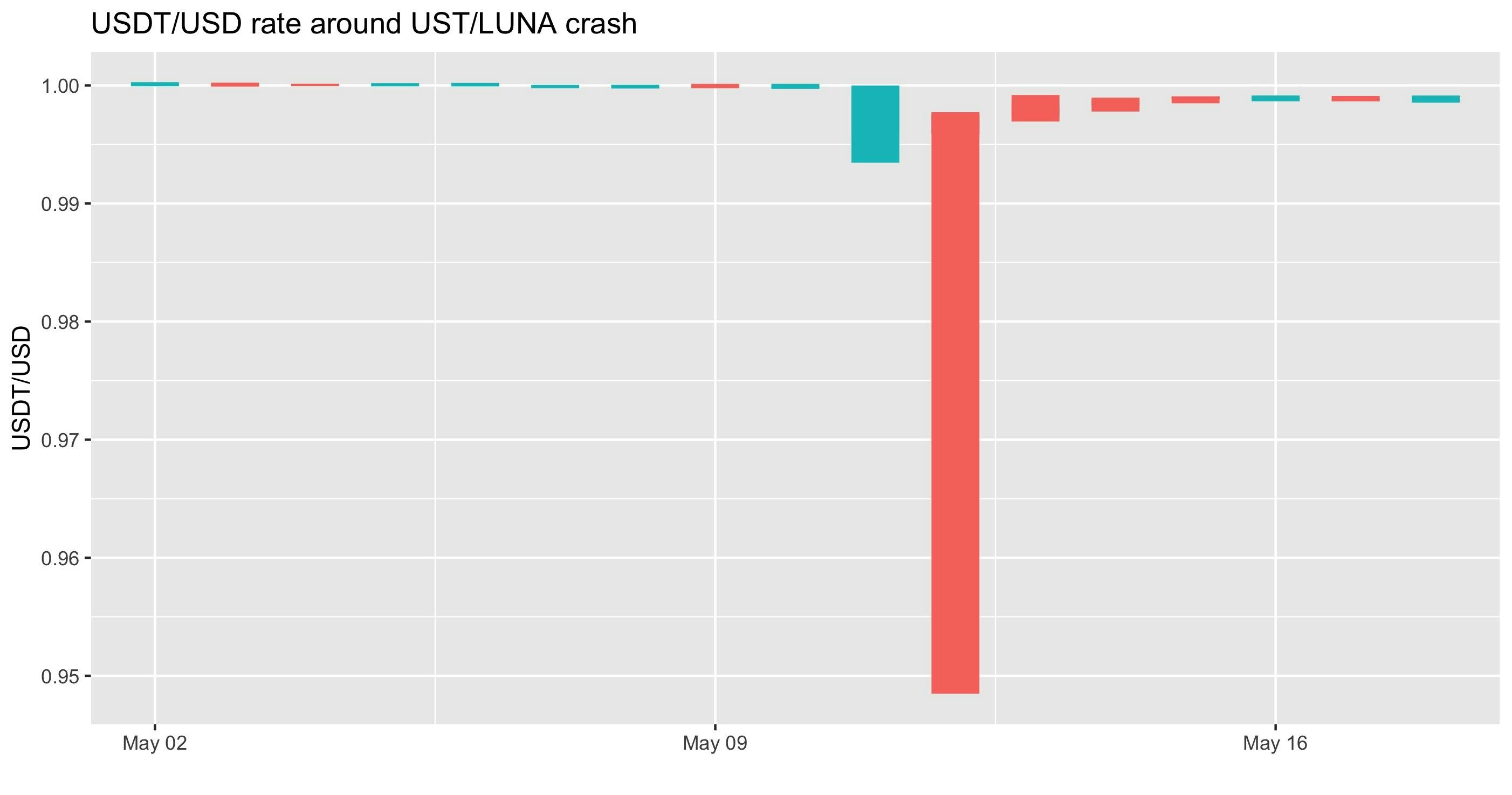

Following the crash of UST, Tether Holdings Ltd experienced a massive redemption wave of around $9B.

This had a visible effect on the market capitalisation of USDT.

Besides a drop in market capitalisation, the redemptions caused USDT to temporarily lose its peg between May 11 and May 13 2022, which is something the stablecoin is yet to fully recover from, and has many questioning its liquidity.

Liquidity health assessment

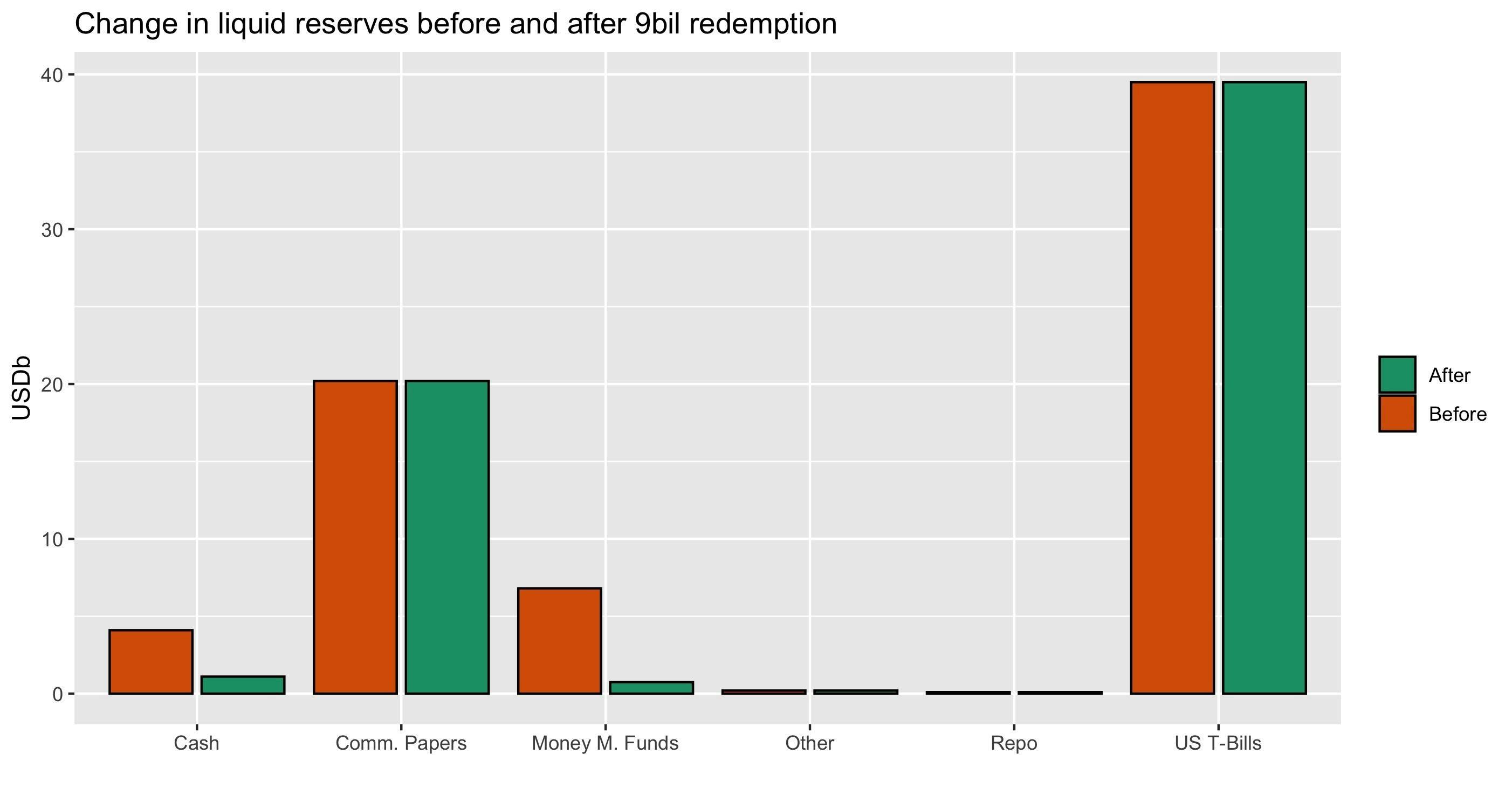

As the state of USDT's liquidity is not very clear, we decided to take a deep dive into Tether Holdings Ltd's latest financial statements (as of March 31, 2022) after we deduced the $9B in redemptions.

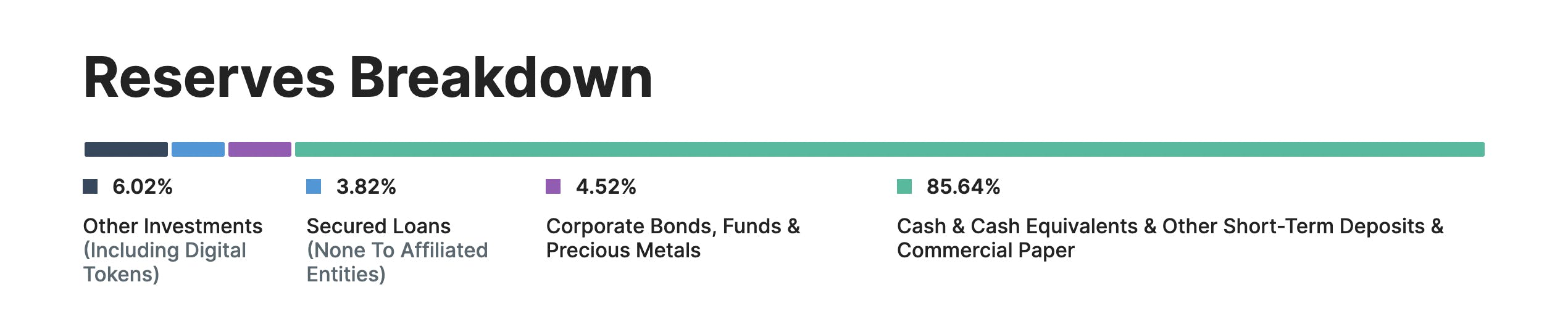

According to those financial statements, Tether Holdings Ltd's reserves are composed of:

- Secured loans

- Corporate bonds, funds and precious metals

- Cash and cash equivalents

- Other investments

What falls under "other investments" is not exactly clear; we can only assume that they may include digital tokens. This means that the only readily available liquidity comes from "cash and cash equivalents".

We looked at the percentage composition of "cash and cash equivalents" provided in the most recent audited financial reports from two periods:

- The week before the $9B redemption wave started (May 5, 2022)

- Right after the redemption wave happened (May 18, 2022)

We also assumed that the redemptions were done using cash deposits ($3B with $1B left as liquidity) and money market funds ($6B).

All this allowed us to create a graph that visually represents the change in liquid reserves before and after the redemption wave.

From the graph, it's easy to see that Tether Holdings Ltd's liquid reserves could be nearly depleted. In case of a new wave of redemptions, the next assets that would have to be used are:

- Commercial papers (short-term debt issued by corporations) and certificates of deposit (negotiable short-term deposits issued by financial institutions) - commercial papers and certificates of deposit both have an average maturity of 44 days, so they would not necessarily be readily available.

- US T-Bills (US Treasury bills with a maturity of less than 120 days) - we do not know the maturity of these bonds, but we can safely say they do not represent readily available liquidity. Also, the only way to convert these bonds into cash is by selling them on the open market. Given the Federal Reserve interest rates hike program, it is likely that these bonds have lost value.

Bank run

While it is true that Tether Holdings Ltd was able to survive the $9B redemption wave, even though it led to its cash reserves being nearly depleted, the real question is, would it be able to survive a similar one? And if yes, how would it affect USDT holders?

If such an event were to happen, we believe there are two possible ways the company would react:

Using speed

Tether Holdings Ltd commits to meet all redemption requests by selling some of its liquid (but not cash equivalent) assets. A portion of these assets could be sold at a discount. As a result, the company's reserves would be worth less than the USD amount of USDT it emitted.

This may leave USDT holders nervous, and confidence in Tether Holdings Ltd may be lost, leading to more redemptions. In a situation of this sort, the company could see removing USDT from the market (buying it below parity) by quickly liquidating its reserves, even at a loss, as convenient. This would be acceptable as long as USDT is trading at sufficient discounted levels.

Eventually, the remaining outstanding USDT would again go back to being fully collateralised, and parity could be reached again.

Using patience

Faced with mass redemption, Tether Holdings Ltd decides to cap the daily maximum of redeemable USDT or even stop redemptions due to liquidity constraints. Investors then get really worried (they fear the company is lying about its reserves) and start dumping USDT on the secondary market (e.g. crypto exchanges), leading to USDT losing its peg.

Given that USDT is (theoretically) fully collateralised, arbitrageurs would have an incentive to buy USDT at a discount on the market, wait for redemption at par, and cash in the difference. Tether Holdings Ltd could also step in and buy back USDT at a discount while liquidating its reserve to face the incoming redemptions.

In both the above-described cases, it's clear that those who have access to the mark-to-market value of USDT reserves can perform an arbitrage. The only people with such access are the ones at Tether Holdings Ltd, giving them an unfair advantage.

Will USDT change for the better?

Although we have mostly focused on the risks of USDT, it's only fair we mention some positives, too, as there appears to be good news regarding the stablecoin.

Strengthening of the reserves

If communications made by Tether Holdings Ltd are to be believed, the company is striving to improve the strength of its reserves. To be more specific, it has reduced the number of commercial papers and increased the number of US T-Bills as well as money market funds within the reserves.

Holdings in commercial papers went down to $20B from $24B (quarter on quarter). Positively adding to this is the fact that the average rating of commercial papers and certificates of deposit has gone up from A2 to A1 (the top rating).

Secured loans within the reserves have also gone down by $1B.

Potential new regulations on stablecoins

Regardless of how unpleasant the market volatility caused by the UST crash and temporary USDT depeg was, it will hopefully push regulators to act promptly and provide some rules on stablecoins.

Without the intervention of regulators, we, unfortunately, might see a situation as bad as the UST/LUNA crash. Only this time, a USD-backed stablecoin could be the main actor.

Key takeaways and recommendations

Using this article, we did our best to present to you the risks that come with USDT. Do keep in mind that having only Tether Holdings Ltd's superficial audited financial report makes it quite impossible to precisely evaluate USDT's liquidity and ability to face a new wave of redemptions.

Still, according to our analysis, Tether Holdings Ltd's cash-like reserve might have been drained by the recent $9B redemption wave. This is quite alarming as a major USDT depeg event (i.e. large and prolonged in time) would have devastating consequences on the crypto market, given that USDT is used as the base currency on some of the largest exchanges (e.g. Binance). It would also erode investors' confidence since there is little use for an unstable stablecoin.

So, what can you do to mitigate risk? A few things:

- Be prepared for volatility - market sentiment on USDT is everything but positive, and its peg to the USD has not been fully established; thus, some volatility is expected.

- Consider converting to USDC - investors who are not willing to accept the risk of even a small and temporary depeg should not have USDT in their portfolio and would be better off converting their USDT into safer stablecoins like or USDC, at least in the short term. On the other hand, investors with a high-risk tolerance could benefit from the higher APY on USDT as opposed to USDC.

Conclusion

All in all, crypto enthusiasts, including ourselves, hope that the peg will be reestablished and Tether Holdings Ltd will be more transparent about the state of its reserves. If this were to happen, USDT would again be a safe choice.

If not, and if USDT causes a systemic shock, regulators will likely step in. This would eventually prove beneficial to the crypto market as a whole.

Which scenario will play out? Only time will tell.